Top 200 furniture manufacturers worldwide: competition in the world furniture industry

CSIL analyses the competition in the world furniture industry, mapping and studying the performance and features of a wide range of furniture companies. More than 8,000 companies operating in different furniture segments are analyzed thanks to comprehensive desk and field research. This supports CSIL in accurately studying the industry’s competitive systems worldwide and monitoring their evolution.

THE TOP 200 FURNITURE MANUFACTURERS BY CSIL

In its recent study ‘Top 200 Furniture Manufacturers Worldwide’, CSIL listed the largest companies in terms of furniture turnover. This group of companies produces a total turnover of around USD 180 billion, of which nearly USD 120 billion, according to CSIL estimates, is related specifically to the furniture sector.

The concentration ratio of the Top 200 furniture manufacturers in the world furniture industry has continued to increase in the last years, reaching more than 20% of world furniture production. The average company’s size in terms of total turnover has also increased, with differences across different geographical areas.

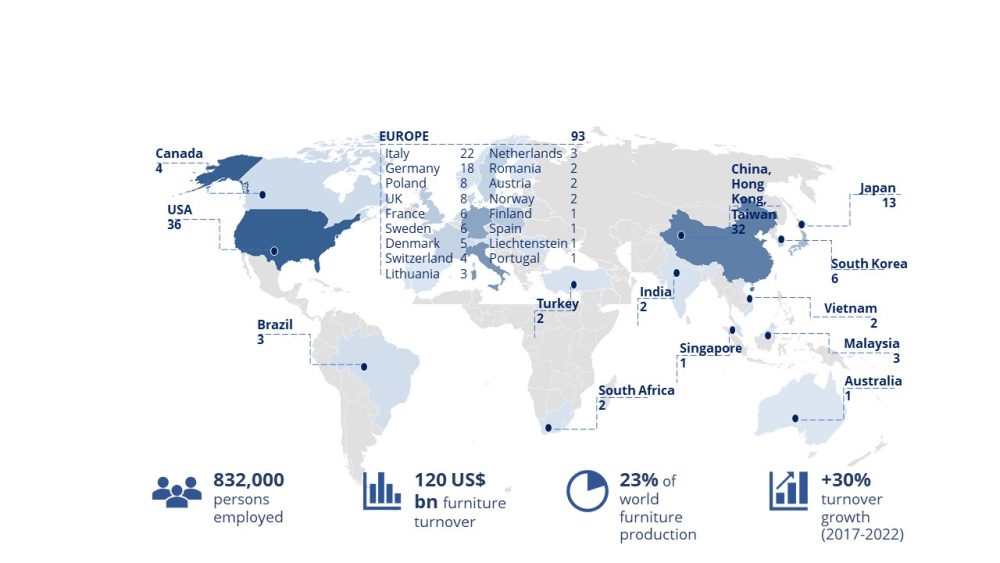

The Top 200 are spread all over the world. They have headquarters in 30 countries. Regarding furniture turnover, top companies from Asia and the Pacific account for nearly 40% of the total furniture turnover generated by the top 200 companies. European and Americas companies account for 30% each.

COMPANIES’ PERFORMANCE

The total turnover of the Top 200 furniture manufacturers increased by over 30% from 2017 to 2022 (more than compensated for the pre-pandemic level). The trend indicates that the growth of the Top 200 companies was higher than that of the sector in terms of sales.

In 2020, the decrease in sales of the Top 200 manufacturers had been contained compared to the world furniture production, driven by larger financial capabilities that allowed leading companies to quickly re-align business strategies, implement new sales channels (e.g. online), and reposition their supply chain.

Preliminary results show that in 2022, the Top 200 companies maintained the same level as in 2021, whereas world furniture production decreased by 3%. Their performances differ accordingly to the geographical areas and the furniture segments. Asian manufacturers have grown impressively over the last five years. European players have shown promising results, particularly in 2021 (surpassing the pre-pandemic level). North American manufacturers experienced significant development in 2019 and stabilized in 2021.

Regarding furniture segments, the most dynamic manufacturers belong to the kitchen and upholstered furniture segments, which have continued to grow in the period considered. Office furniture manufacturers showed a significant drop in 2020 and a slight increase in 2021 without reaching the pre-pandemic level.

COMPANIES’ STRATEGIES

Strategies of delocalization and differentiation of companies’ manufacturing footprint have been accelerated over the last few years, driven by an increasing need to contain logistic and transport costs, reducing the time-to-market.

About half of the Top 200 companies have manufacturing activities outside their headquarters country. Companies that mostly delocalize part of their production abroad have headquarters in North America, followed by Asian manufacturers and European companies.

In terms of furniture segments, companies specializing in outdoor furniture are the most prone to delocalize production (80% of the companies selected opened manufacturing plants abroad), followed by companies specializing in office furniture and upholstered furniture manufacturing.

About 80 M&A operations have been identified among the Top 200 furniture companies since the beginning of 2019, averaging 20 significant operations per year. American and Italian companies were the most active in recent years, concluding around 40 M&A operations among the sample of the Top 200 companies, followed by companies headquartered in China and the United Kingdom.

Over the period, the most active American companies observed have been two office furniture specialists: Herman Miller, which acquired Maars (NL), HAY (DK), and Naughtone before finally merging with Knoll, and Steelcase, which also made 4 acquisitions since 2019. In Italy, different operations have been concluded among leading highend furniture manufacturers. IDB Italian Design Brands was the most active company, with 4 acquisitions. Another Italian high-end furniture group, Design Holding, was also actively acquiring foreign companies with a strong presence in Northern Europe and North America: Company (DK) and YDesign Group (US).

Since 2019 there have been three significant mergers between the Top 200 companies. The first occurred in 2020 when ACProducts merged with Masco Cabinetry to form Cabinetworks Group, now one of the largest global cabinet/kitchen furniture manufacturers.In 2021, Alsapan and P3G Industries merged to form Alpagroup, a leader in RTA furniture production. In the US, the two office furniture giants Herman Miller and Knoll merged to form MillerKnoll, now the largest office furniture manufacturer in the world (in terms of turnover).

ABOUT THE COMPANIES FIGURES

CSIL constantly updates a comprehensive set of companies’ information, including financial figures, employment, export sales, and product portfolio, supported by different sources of information: an extensive database of companies that includes historical data on main financial indicators; annual reports of companies quoted on the stock exchange; specialist sector press, companies’ websites, and press statements; CSIL’s field research, including online surveys and direct interviews conducted during the year.